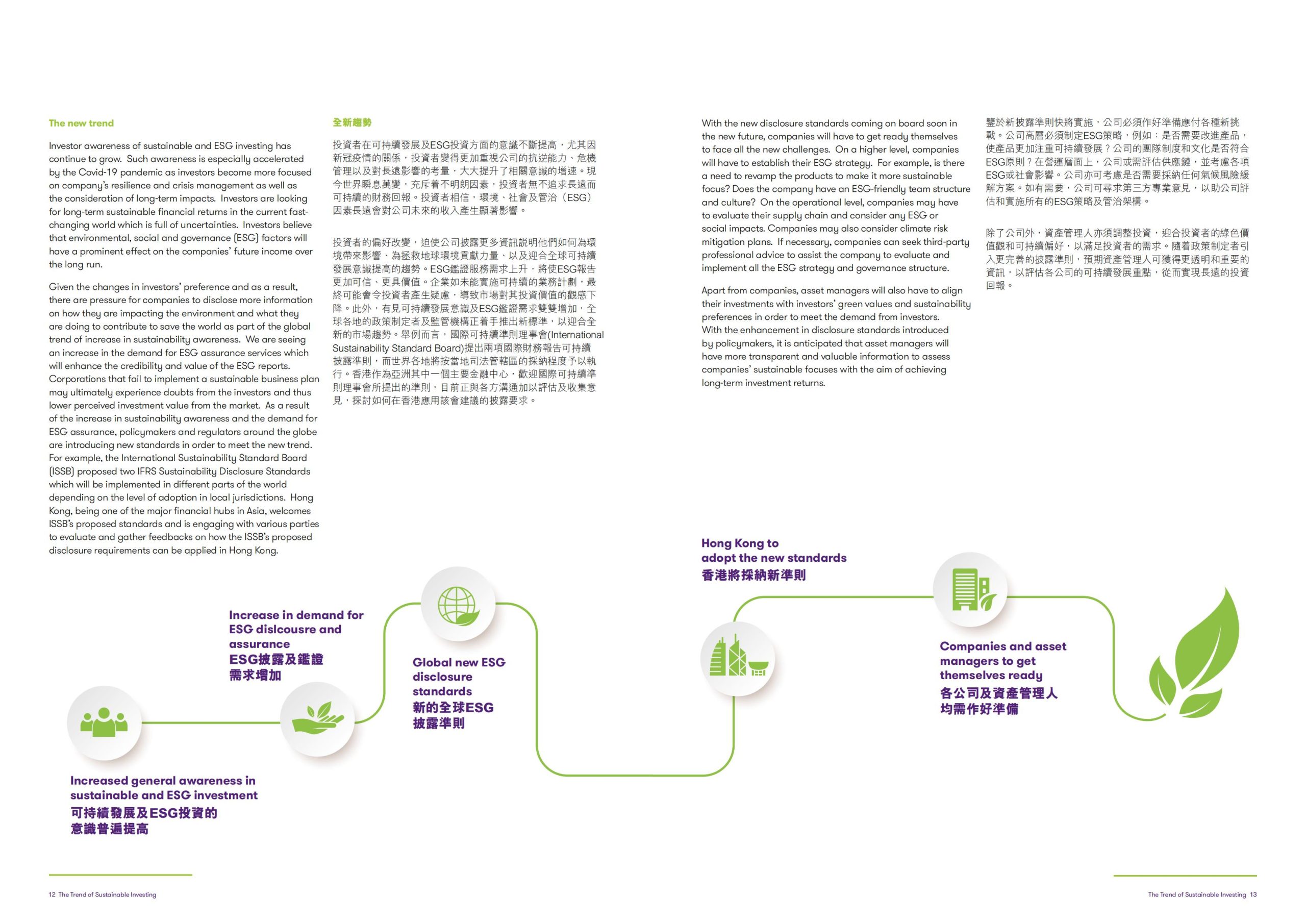

The proposals were built on recommendations from the TaskForce on Climate-Related Financial Disclosures [TCFD].These proposals also incorporated industry-based disclosurerequirements derived from Sustainability Accounting StandardsBoard [SASB] Standards.

The ISSB sought comments on the two proposed IFRS

Sustainability Disclosure Standards and it aims to finalise therequirements by the end of 2022.

The proposed IFRS S1 General Requirements for Disclosureof Sustainability-reloted Financial Information [General

Requirements Exposure Draft] requires companies to discloseinformation about all of their significant sustainability-relatedrisks and opportunities.

The proposed IFRS S2 Cimate-related Disclosures [ClimateExposure Draft] focuses on climate-reloted risks and

opportunities.It incorporates the recommendations of the TaskForce on Climate-related Financial Disclosures [TCFD] andincludes metrics toilored to industry classifications derived fromthe industry-based SASB Standards.

是項議案以氣候相關財務披露工作小组(Task Force on

是項議案以氣候相關財務披露工作小组(Task Force on

Climate-Related Financial Disclosures)的建議作為基礎,业已納入根據可持績會計凖則委員會(Sustainability AccountingStandards Board)凖則所得出的行業披露要求。

國際可持續凖則理事會已就兩項建議中的國際財務報告可持續披露凖則廣纳意見·业致力於2022年底落實相開凖則。

建議的國際財務報告可持續披露凖則第1號——可持續發展相關財務資訊的一般披露要求《一般要求徵求意見稿》要求公司披露所有有關重大可持續發展風險和機遇的資訊。

建議的國際財務報告可持續披露凖則第2號——氣候相開披露《氣候徵求意見稿》著眼於舆氣候相開的風險和機遇,當中不但納入了氣候相關財務披露工作小組的建議,亦包括針對行業分類而特設的指標,有關分類是根據可持續會計準則委員會按行業劃分的凖則訂立。

本文来自知之小站

报告已上传百度网盘群,限时15元即可入群及获得1年期更新

(如无法加入或其他事宜可联系zzxz_88@163.com)